In a recent Memorandum of Understanding signed by the Federal Inland Revenue Service (FIRS) and the Lagos Internal Revenue Service State (LIRS), both agencies have agreed to a collaboration and unification in the areas of tax audit, tax collection, capacity building and exchange of taxpayer information.

While this move is a good development that gradually introduces tax harmonisation to eliminate multiple taxation or multiple tax audits by both agencies for Lagos taxpayers, it importantly implies that corporate taxpayers in Lagos State will have little hiding place from tax.

Taxpayer data will become easily available to both tax authorities, as information exchanges take place.

The FIRS will exchange all the taxpayer data in its purview, including data from international tax information exchanges pertaining to Lagos taxpayers, while LIRS will do the same, including for all those businesses in the informal sector who are not in FIRS’ tax net.

For more information about how this Joint Agreement can affect your business interests in Lagos State, please do not hesitate to send your enquiries to clients@vi-m.com.

As the case for constitutionality of Value Added Tax (VAT) and the appropriate authority for its collection and administration continue to rage, we deem it important to highlight the following considerations for Nigerian businesses (based on the provisions of the VAT laws already drafted/ issued by Rivers, Lagos and Ogun States), just perchance the case for VAT collection is ruled eventually by the Supreme Court in favour of the State governments:

As should be expected, businesses will need to learn and practice all the various State VAT laws applicable in the States where they carry on business.

More businesses will be brought into the VAT net as the State governments would be much more aggressive towards collecting VAT.

States may have different VAT rates (as is already the case with Lagos State) – this will mean different prices for the same goods and services across different states. If the price differences are significant, customers may incline to States with lower prices and the business terrain will become much more competitive.

Businesses will need to register for VAT and pay/ file VAT monthly, to the State or respective States where they have office/ branches and from where supplies are made.

Online or e-commerce businesses will need to register and pay/file VAT in the place of business/ company registration, and in other respective States from where supplies of goods are made.

Non-residents carrying on business in Nigeria would also need to register for VAT in the various States where they have subsisting contracts with customers. Their Nigerian customers will be expected to become the State’s agents for collecting/ filing VAT on behalf of their non-resident suppliers/ contractors in the currency of the transaction.

VAT exemptions already in place in the national VAT act, e.g. exemption of small businesses from VAT, may not be available with the States.

The accounting systems of businesses will need to be reconfigured (this will require more work where the business has various branches in different states), to take cognisance of new VAT registration numbers, new VAT rates, VATable/exempt/ zero-rated goods and services, transactions with non-residents and sales/ cost of sales – for calculating output and input VAT (and for respective State branches, where applicable).

Businesses may be asked to pay VAT at the various State borders whenever there is shipment of goods into or across a State (States may adopt this mechanism for collecting ‘VAT on imports’ as is already contained in some State VAT laws, since VAT on imports are already being collected by Customs at the National ports / borders). This means there may be multiple layers of VAT, payable by businesses within their supply chains. If the Federal government is eventually restrained by the courts from collecting VAT on imports, States without import borders/ ports may resort to this measure to generate more revenues.

Cost of VAT compliance/ accounting, and consequently, cost of doing business will go up.

For trading businesses, claim of input VAT may become challenging especially where it is paid in another state (unless there will be some sort of input VAT MOU among States) or where input VAT paid is higher than output VAT charged. The same issue will arise where the goods are imported into Nigeria and the associated VAT is paid to Customs (unless the Federal government would be restrained from collecting VAT at the point of clearing imported goods).

Accounting (and tax accounting) will become more complex for businesses, especially those operating in more than one State, and/ or where the rates of VAT differ among the States where they operate.

Businesses will be required to stop using Federal Inland Revenue Service (FIRS)’ taxpro-max platform for filing VAT returns and will need to start learning/ adopting the compliance methods or platforms as will be prescribed by the State or respective States where they operate.

Businesses with outstanding VAT refunds from the FIRS will not be able to apply it for offset of their future VAT liabilities. It may also become much more challenging to get such refunds in cash from the FIRS.

Tax disputes between the taxpayers and the tax authority are to be referred first to State tax appeal tribunals (TAT). Since the State TATs would be centralised within the respective States, possibility of full autonomy from the control of the State governments may be limited, creating a situation where it may be very difficult for taxpayers to win any tax dispute against the State tax authority.

As at 14 September 2021, Rivers State, through its Attorney-General, had appealed to the Supreme Court to set aside the decision of the Court of Appeal that ordered it to maintain status quo on the collection of VAT, pending the determination of an appeal that was lodged by the FIRS.

For further enquiries about VAT or the progress of the case, or how all of these may affect your business, please do not hesitate to send an email to clients@vi-m.com.

Yesterday, 17 September 2020, the Federal Inland Revenue Service (FIRS) issued a Public Notice, directing ALL account holders in Financial Institutions (Banks, Insurance Companies, etc) to obtain, complete and submit ‘Self – Certification Forms’ to their respective Financial Institutions.

The same directives were sent out through a series of tweets from @NigeriaGov, the twitter handle of the Federal Government of Nigeria.

Both the FIRS and the Federal Government have now apologised for this directive, clarifying that the ‘Self-Certification form’ is largely for foreigners or people with dual citizenship/ residency, holding accounts with Financial Institutions in Nigeria.

The forms are required by the relevant financial institutions to carry out due diligence procedures in line with the ‘Income Tax (Common reporting Standards) Regulations, 2019.

The ‘Income Tax Regulations’ deal with reporting for financial accounts held by foreigners or people with dual residency in Nigeria. The banks/ financial institutions are required to perform due diligence to identify ‘Reportable Accounts’ (that is accounts of foreign persons to aid Automatic Exchange of Information with other countries) and then submit such reports in the required format, to the FIRS.

However, somewhere in the Regulations, FIRS is still empowered to check all other accounts of the banks/financial institutions to verify that they actually did the due diligence right and submitted all the correct ‘Reportable Accounts’.

Just to stay safe in case of any such unexpected requirements by the tax authorities, we recommend that all taxpayers do their possible best to stay at the right side of tax at all times.

In a series of tweets from its twitter handle (@NigeriaGov) earlier today, 17 September 2020, the Federal Government of Nigeria informed the general public that all account holders in Financial Institutions (Banks, Insurance Companies, etc) are required to obtain, complete and submit Self – Certification Forms to their respective Financial Institutions.

The forms are required by the relevant financial institutions to carry out due diligence procedures in line with the ‘Income Tax (Common reporting Standards) Regulations, 2019.

The self-certification form is in 3 categories: –

Form for Entity.

Form for Controlling Person (Individuals having controlling interest in a legal person, trustee, etc).

Form for individual.

According to the tweets, failure to comply with the requirement to administer or execute this form attracts sanctions which may include monetary penalty or inability to operate the account.

No effective date or deadline for collection and submission has yet been announced. Enquirers are currently referred to firs.gov.ng.

Yesterday, 5 August. 2020, we at Vi-M Professional Solutions held a webinar on ‘Stamp Duty as it impacts Nigeria’s Real Estate sector’.

The following tax men joined our Partners on the webinar, to provide the Revenues’ positions on the operation of Stamp Duties in Nigeria:

1. Mr. Mathew Sanya Gbonjubola (Director, Tax Policy at the Federal Inland Revenue Service) 2. Mr. Waidi Ogunnorin (Lagos State Commissioner for Stamp Duties)

For those who missed the webinar, Here is the live recording on YouTube:

Some takeaways from the webinar include:

1. Most of the Stamp Duty rates being charged in practice, particularly by the FIRS, are JTB harmonised rates from 2002 (according to the Tax Policy Director), which are much higher than the rates actually stipulated by the Stamp Duties Act (SDA) of 2004 as amended.

2. These JTB harmonised rates have not been signed into law nor gazette, meaning that the provisions of the SDA still hold legal pre-eminence over them, until such a time that the laws are amended or signed, to reflect them.

3. Consultations with stakeholders are on-going, to agree on more realistic rates and amend (and gazette) the SDA accordingly.

For further enquiries, please contact us via clients@vi-m.com. Also visit www.vi-m.com/webinars to register for any of our training courses.

Stamp Duty (SD) is a type of tax that is applicable on the execution of certain instruments and special documents. For example, Receipts, Agreements, Contracts, Title deeds etc., to give it additional legal backing and enforcement in the event of dispute or presentation at a court of law, to make it enforceable.

Stamp Duty Act (SDA) is an Act to provide for the levying of stamp duties on certain matters / documents. It is the Act that gives the enabling government agency (Federal Inland Revenue Services (FIRS) for all federal related transactions and the State Internal Revenue Services (SIRS) for all state related transactions).

It therefore means that the first starting point for anyone or businesses is to determine if an instrument is liable to SD and thereafter to which tax authority – to the FIRS or to the SIRS.

It is also important to note that the existence of the SDA preexists Nigeria’s independence and as such it is here to stay, following the renewed efforts, commitment and focus by the FIRS and in view of the huge internally generated revenue that is attributable to this tax type.

It is on record also, that the total amount of SD collected for the calendar year 2019 is about NGN18billion, while for the first five (5) months (January to May) of 2020 the agency has recorded about NGN66billion in revenue.

CHANGES / REMINDERS TO THE GENERAL PUBLIC:

The FIRS is the competent authority to charge and collect SD upon instruments relating to transactions or matters executed between corporate bodies or between a corporate body and an individual, group or body of individuals, while the relevant SIRS shall collect SD in respect of instruments executed between individuals at such rate to be imposed or charged in agreement with the Federal Government.

Following the huge revenue attributable to this tax type and the changes in the Finance Act 2019 (which broadens the scope / complexity of this tax type), the FIRS has introduced and clarified the following as liable to SD:

All written / printed dutiable instruments or receipts

All electronic dutiable instruments or receipts (i.e. in the form of electronic media content, electronic documents or files, e-mails, short message service (sms), instant messages (IM), any internet-based messaging service, website or cloud-based platform, etc.)

All printed receipts (including POS receipts, physicalized device receipts, Automated Teller Machine (ATM) print-outs and other forms of written or printed acknowledgment)

All electronically generated receipts and any form of electronic acknowledgement of money for dutiable transactions

The FIRS issued a comprehensive Information Circular in May 2020, to explain and clarify the practical implications of the provisions of the Finance Act, 2019, regarding SD. This Information Circular can be found and downloaded here.

FIRS had also developed and launched an online portal “Integrated Stamp Duty Services” to support the activities of the agency. This portal – https://stampduty.gov.ng/ affords closer interactions, payments and issuance of stamp duties certificates / receipts to the taxpayer right from this platform.

For ease of administration, there are basically two (2) types of stamp duty payments. The fixed rate and the Ad Valorem rate (a percentage of the value indicated on the instrument to be stamped).

Historically, Stamp Duties were chargeable on only physical instruments but with the advent of the Finance Act, 2019, it now covers electronic transactions as well.

Following this, the apex revenue agency in Nigeria has also launched the FIRS adhesive stamp for the sole purpose of the SDA and calls on all taxpayers to adhere and utilize this, which is available in all of the FIRS offices nationwide.

In the same swift vein, the agency has setup an Inter-ministerial committee effective 30th June 2020, charged with the responsibility to audit and recovery five (5) years’ stamp duties charges from relevant government agencies and MDA’s. Members of the committee includes persons from Central Bank of Nigeria (CBN), Federal Ministry of Justice, the FIRS as well as Ministry of Finance, Budget and National Planning. This committee is to review the financial records of relevant government agencies, ministries, parastatals and establishments that collects stamp duties but are yet to remit same to the FIRS.

For the avoidance of doubt, the following amongst others are instruments liable to Stamp Duty:

FIXED DUTY INSTRUMENTS

AD-VALOREMINSTRUMENTS

Receipts / Guarantor’s / proxy forms

Sales Agreement

Power of Attorney

Contract notes

Certificate of Occupancy ( C of O)

Insurance policies

Memorandum of Understanding

Promissory notes

Ordinary Agreements

Deed of Assignment

Joint Venture Agreement

Tenancy / Lease Agreement

Instruments or documents executed outside of the country and received in Nigeria are also liable to SD, following the conditions mentioned below:

If such instrument is retrieved or accessed in or from Nigeria

If such instrument stored in a device such as a computer/hard drive and brought into Nigeria

If such instrument is stored on a device, server or a computer in Nigeria

CONCLUSION

The creation of the SD portal by the FIRS is aimed and streamlining activities for the tax payers going forward. It is therefore easier for anyone to go online in from any location in the world to pay for and obtain receipt / certificate to confirm that an SD has been paid for an instrument. In some cases, these document might not be physically stamped, but payment and collection of certificate then implies that the right thing has been done on the said instrument.

While in a situation and an adhesive need to be fixed on an instrument, the taxpayer can approach the closest FIRS office to his or her location to pick-up the necessary adhesive and ensure compliance.

It is expected that over the next few months, we would begin to see more attention and activities from the committee that has been setup to audit and recovery five (5) years’ stamp duties.

Organizations and persons carrying on business in Nigeria now need to review each and every of its transactions and instrument with a view to ensure compliance so as to ensure compliance with the SD. Failure to comply may lead to penalty charges of various degrees, prosecution or both. Further, legal documents not properly stamped will not be admissible or held valid in the court of law, including contracts of employment.

We at Vi-M Professional Solutions are available to assist review your records and transactions and give you a report stating your compliance levels in connection to the provisions of the SDA. Please contact us at clients@vi-m.com, should you require any further clarifications on the issues stated above or if you require any assistance in this regard.

The views expressed in this article are Vi-M’s general overviews of the enabling legislations on SD and practical activities of the FIRS. We encourage you to contact our representatives one-on-one through www.vi-m.com or clients@vi-m.com should you intend to take any action, implement any changes or make payment for stamp duties on account of this article.

The Federal Inland Revenue Service (FIRS) has released new Value Added Tax (VAT) filing forms 002 – (for headquarters and branches); and 006 – (for self charge or withholding of VAT), respectively. The forms can be viewed or downloaded here.

In the FIRS’ bid to ease the difficulty of filing VAT (particularly for large, multi-location businesses), these forms have been designed separately to include forms for Head office, Branch offices and Self charge (in the case where the business is not issued a VAT invoice by its supplier).

These new VAT filing forms are to replace the old form and has been reviewed to incorporate the changes made in the Finance Act, 2019. On filing/submission (through online or offline platforms) to FIRS, the new self-charge VAT form 006 should be accompanied by a schedule of all the suppliers of goods or services from which the business has withheld VAT or on whose transactions the business has self-charged itself VAT (that is, where the business was not issued a ‘VAT invoice’ by its supplier based on the provisions of the Finance Act 2019).

Comments

The introduction of the new VAT filing forms (form 002) for Head Office and Branch offices, albeit bringing a bit of controversy as to whether branch operations are now independently taxable in Nigeria, will ease the difficulty and late filing of VAT by allowing divested tax functions and taking advantage of proximity between the VAT offices and business premises.

FIRS would also be able to track the inflow of VAT from Head office, Branch offices, and Self charge/ withheld VAT, giving them a better picture of how VAT was remitted to avoid tax evasion, particularly for the Self charge cases.

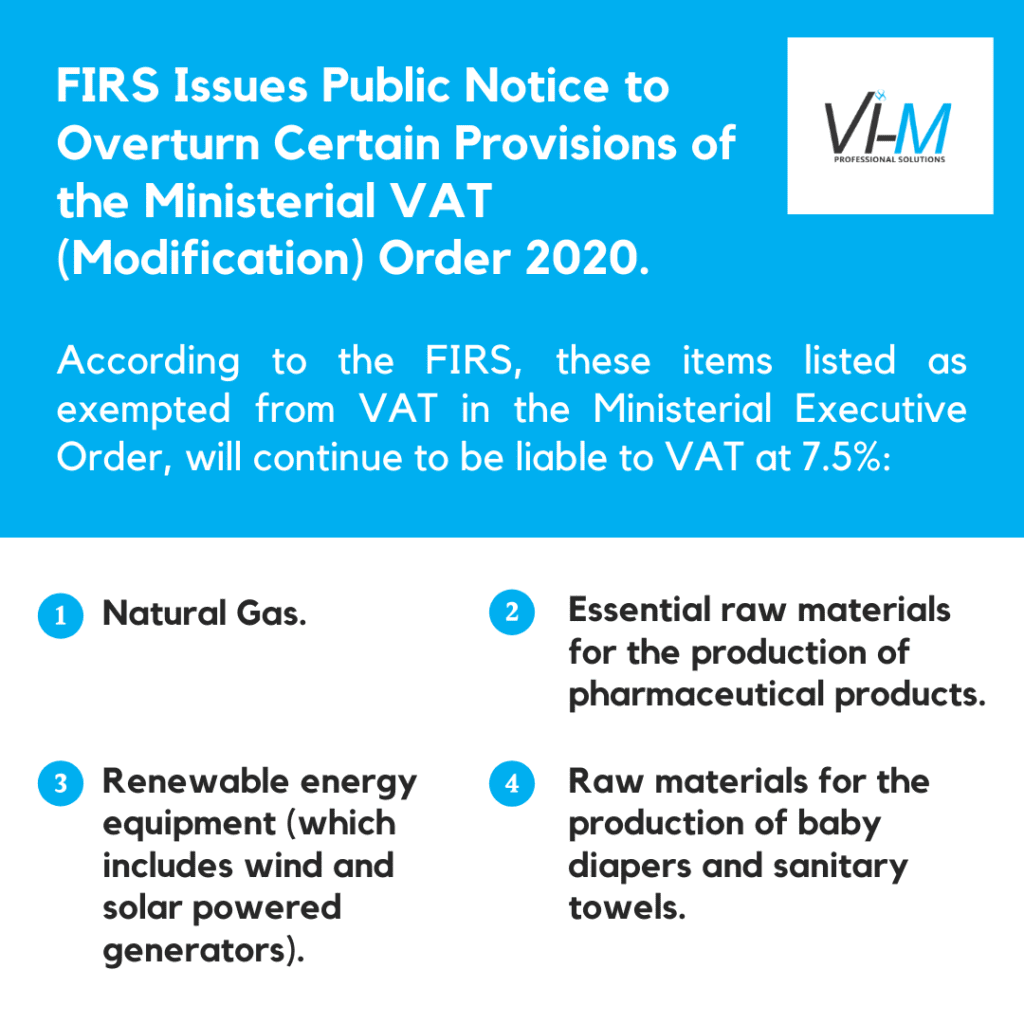

On Wednesday, 24 June 2020, the Federal Inland Revenue Service (FIRS), issued Public Notices in the Newspapers, overturning the Value Added Tax (VAT) Exemptions granted to some items in the Value Added Tax (Modification) Order 2020, which was issued by the Minister of Finance, Budget and National Planning in May 2020.

These items include:

Natural Gas (which is a crucial component, required in most major sectors of Nigeria’s economy, e.g electricity generation, manufacturing, domestic use, fertiliser production, etc.)

Essential raw materials for the production of pharmaceutical products.

Renewable energy equipment (which majorly includes wind and solar powered generators).

Raw materials for the production of baby diapers and sanitary towels.

FIRS, in its Public Notice, argues that these items cannot be made VAT exempt by the VAT (Modification) Order as they were not listed on the 1st Schedule to the VAT Act, neither were they listed in a previous Ministerial Order.

The FIRS insists that these items will continue to be liable to VAT at 7.5% until otherwise provided in an appropriate statutory instrument.

Our views:

First: The VAT (Modification) Order, 2020 firstly modifies the provisions of Schedule 1 of the VAT Act and then goes ahead to provide extended list/ interpretations for the all the items (as modified). FIRS’ argument on these items not being listed earlier in the VAT Act or in a previous Ministerial Order, may not therefore hold strongly.

Second: Not all provisions of the VAT (Modification) Order 2020 are favourable to taxpayers or align with the earlier provisions of Schedule 1 to the VAT Act.e.g. the non-exemption given to basic food items sold in hotels, eateries and similar places and those supplied by caterers / contractors; baby products for children above 3 years old; and educational materials not used in conventional schools. Overturn to all these provisions therefore ought to be made uniformly, and not just to selected items.

Third: The overturned exemptions relate to items that are essential goods for powering the major essential sectors of the economy. These items are continuously supplied in large quantities in Nigeria and their exemptions from VAT would cause a huge dip in tax revenues. In its endeavours to increase tax revenues collection, this may well be the major reason why FIRS overturns the VAT exemptions on these items.

Fourth: Government should work towards harmonising all the divergent interpretations on such issues; for simplicity, ease and certainty of taxes in Nigeria, even as businesses and income earners struggle against the pandemic, the global economic decline and all other odds to protect their income and asset bases.

On 2 June, 2020, the Federal Inland Revenue Service (FIRS) issued 3 public notices to taxpayers.

Here are the highlights:

Public Notice 1: The FIRS is further extending the deadline for settling outstanding tax liabilities from self assessments, tax audits/investigations/ reviews and VAIDS from the earlier provided deadline of 31 May 2020, to 30 June 2020. FIRS, by this Public Notice, is asking taxpayers owing any such taxes to settle on or before 30 June 2020 in order to qualify for waivers of interest and penalty.

Public Notice 2: The FIRS is asking all Nigerian and non-Nigerian businesses to keep proper accounting records in English language or risk penalties according to the tax laws.

Public Notice 3: The FIRS is to resume activities relating to previously done tax audits, immediately. Field visits for tax audits/ investigation/ monitoring to resume on 30 June 2020.

For further enquiries or help with your tax concerns, please contact us via clients@vi-m.com

Earlier in the year, the Federal Inland Revenue Service (FIRS) issued a Public Notice to announce the coming into effect of the VATrac- An Automated VAT Filing and Collection platform which would be compulsorily used in the wholesale/ retail sector and for direct audit/ reconciliation of of VAT transactions.

Affected businesses include branded shops, super stores, general supermarkets, standard restaurants; and eateries. These businesses are required to include in their transaction/ sales receipts the following:

FIRS or JTB TIN;

Print date;

Goods/ product description;

Receipt Number;

Grand total;

Standard 7.5% VAT rate

VATrac was expected to have taken effect from 1 April 2020 and affected businesses have been asked to contact the nearest FIRS tax office for onboarding on VATrac. Further directives on the practical implementation/ use of the VATrac are however still being awaited from the FIRS .

Businesses that would be affected by this new platform, namely, branded shops, super stores, general supermarkets, standard restaurants; and eateries are advised to prepare themselves for using an automated VAT system by staying abreast of retail related accounting software and automating their selling processes with a dependable Point of Sale (POS) software.

Further, the VATrac by FIRS may also be a cloud based platform, necessitating the use of stable internet enabled devices for retail sales.

For help with installing a retail/ restaurant/ eatery Point of Sale or accounting software, please contact us via clients@vi-m.com.

To find out all about VAT and how it works in Nigeria, please refer to our ebook on ‘Value Added Tax Explained‘.