The Finance Act 2020, which came into effect on 1st January 2021, amended Section 18(1) of the Nigeria Export Processing Zones Authority (NEPZA) and Oil and Gas Free Zone Authority (OGFZA) Acts respectively, to make it a statutory requirement for enterprises within the respective zones to file income income tax returns, albeit no income tax is payable.

On this backdrop, the Federal Inland Revenue Service (FIRS) has recently issued a Public Notice, to serve as a guide for enterprises in the Zones to file the required income tax returns.

The Notice stipulates as follows:

- The NEPZA Act and OGFZA Act (as amended) mandate all enterprises registered and operating in the zones to file income tax returns in accordance with the provisions of the Companies Income Tax Act (CITA).

- As such, all enterprises registered and operating in the zones are required:

a. to file income tax returns for 2021 and subsequent years of assessment; and

b. to compute income tax and pay the tax due (if any).

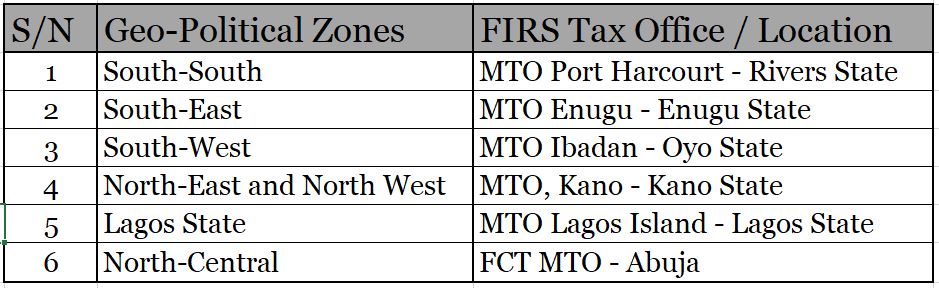

The returns should be in the manner and time specified by CITA. - For ease of compliance, all approved enterprises are required to file their income tax returns at the following FIRS’ tax offices:

a. Enterprises operating in the Zones located in South-South Geo-political region of Nigeria- MTO Port Harcourt;

b. Enterprises operating in the Zones located in South-East Geo-political region of Nigeria- MTO Enugu;

c. Enterprises operating in the Zones located in South-West Geo-political region of Nigeria- MTO Ibadan;

d. Enterprises operating in the Zones located in North-East and North-West Geo-political region of Nigeria- MTO Kano;

e. Enterprises operating in the Zones located in Lagos State- MTO Lagos Island; and

f. Enterprises operating in the Zones located in North-Central Geo-political region of Nigeria and FCT- MTO Abuja. - Relevant penalties prescribed by CITA or Federal Inland Revenue Service (Establishment) Act 2007 shall apply to any company that fails to comply with the filing requirements as regards due dates.

This Notice provides the much needed clarity as to the Expectations of the FIRS, regarding how free trade zone enterprises are to comply with the new amendments to the NEPZA and OGFZA.

For further enquiries or help with filing the income tax returns, please send an email to clients@vi-m.com.